E-commerce in 2026 is reaching new heights, fueled by a post-pandemic digital boom and evolving consumer habits. Online retail sales are projected to account for over 22% of all retail worldwide by 2026, as shoppers increasingly favor the convenience of e-commerce. For online sellers, understanding what products are in highest demand – and why – is crucial for staying ahead of the curve. This comprehensive report analyzes the top-selling product categories expected in 2026 by examining historical data from 2024–2025 and current marketplace trends. We’ll break down performance on major platforms (Amazon, TikTok Shop, Shopify, and Temu), provide regional insights across the US, Europe, Southeast Asia, and Australia, and even forecast quarter-by-quarter trends in 2026. Along the way, we’ll incorporate data-driven charts, rankings, and deep analysis of macro forces shaping consumer behavior – from the AI revolution and the wellness boom to sustainability priorities and the rise of impulse-driven “social commerce.” The goal is to equip eCommerce entrepreneurs and brands with thought leadership-level insight into what will sell best in 2026 and how to capitalize on these trends. Let’s dive in.

Top-Selling Product Categories in 2026

Top global e-commerce categories by online sales in 2024 (Statista). Electronics and fashion dominated in 2024, with food, beverages, and home improvement also in the top ranks. These categories are expected to remain on top through 2025 and into 2026, with some shifting growth dynamics.

Online shopping encompasses virtually every retail category today, but a few product categories consistently lead in revenue. As of 2024, the top categories worldwide by online sales were: electronics, fashion, food (grocery), beverages, home improvement/DIY, furniture, media, beauty & personal care, tobacco alternatives, and toys/hobbies, in that order. Electronics alone accounted for nearly $922.5 billion of online spending globally in 2024 – the single largest slice of e-commerce. Fashion and apparel were a close second at around $760 billion. Food and beverages together also formed a massive segment, as online grocery shopping and delivery became firmly entrenched in consumer habits.

By 2026, these categories are expected to remain on top, but with notable shifts in growth rates and consumer focus:

1. Electronics & Smart Devices

Consumer electronics should maintain the #1 spot in 2026, driven by an ever-expanding range of devices. From smartphones and laptops to smart home gadgets and wearable tech, electronics benefit from constant innovation and global demand. In 2024, electronics online sales were projected around $922.5 billion, and that number has grown year-over-year (18.1% growth in 2024). By 2026, electronics may well exceed $1 trillion in online sales globally (based on mid-teens annual growth). Continued product launches (e.g. next-gen smartphones, VR/AR devices) and consumers upgrading older tech will fuel this category. Moreover, the average order value in electronics is high, boosting revenue – for example, online marketplaces report best-sellers like laptops and TVs regularly in the top-grossing products. Electronics’ strength also spans both essential gadgets (phones, tablets) and niche devices (drones, smart appliances), giving this category a broad base. However, competition is intense and margins can be thinner, meaning sellers will lean on scale and volume.

2. Fashion & Apparel

Online fashion is a powerhouse that will continue to thrive in 2026. In 2024, global fashion e-commerce was about $760 billion, and it’s growing steadily as more consumers buy clothing, shoes, and accessories online. By 2026, fashion’s online revenue could approach the ~$1 trillion mark if growth holds. What’s driving it? The rise of fast fashion and DTC brands, social media-driven trends, and the ease of browsing vast catalogs of styles online. Notably, the fashion category has a high volume of units sold – e.g. 4.5 billion garments were sold online globally in 2024 – but a lower average ticket price (~$45) and high return rates (~25% returns). This indicates shoppers buy lots of affordable apparel online, often in multiple sizes or styles with the intent to return what doesn’t fit. In 2026, fashion will still be top-of-mind, but brands are adapting with more sustainable fabrics and inclusive sizing, as well as leveraging dropshipping and print-on-demand models. One emerging twist is the growth of “collectible” fashion and nostalgia-driven apparel trends on social platforms – for example, TikTok-driven fads like vintage band tees or niche streetwear can explode in popularity overnight. Fashion’s popularity is also regionally ubiquitous – it ranks as the #1 or #2 category in most markets (e.g. #1 in the US by revenue at $163 billion in 2024, and a top category across Europe and Asia as well).

3. Home, DIY & Furniture

The home goods sector (encompassing DIY hardware, home décor, appliances, and furniture) saw strong online growth in recent years. In 2024, DIY and tools accounted for about $220.2 billion and furniture another $220.1 billion in global e-com sales. Combined, this “home & living” super-category rivals food or fashion in size. In 2020-2021, lockdowns caused a spike in home improvement and furniture purchases online. By 2026, some normalization is occurring – for instance, excess inventory in home goods from the pandemic boom is now being heavily discounted (some home goods retailers are offering ~70% off to clear out stock). Still, underlying demand remains robust. Consumers have gotten comfortable buying even big-ticket items like couches or exercise equipment online, especially with AR visualization and generous return policies. The convenience of delivery for heavy items (think having a barbecue grill shipped to your door rather than hauling it from a store) is a lasting advantage. We anticipate continued innovation in this category: smart home devices (robot vacuums, smart thermostats) blur the line between home goods and electronics, driving crossover demand. Ergonomic furniture for home offices and multipurpose furniture for small spaces are trending as work-from-home persists. While growth might be slower than the peak, home goods online sales in 2026 should still trend upward, aided by the real estate market (new homeowners often spur home goods purchases) and a DIY culture amplified by online tutorials. One challenge to watch is price sensitivity – large home purchases often see consumers waiting for sales. Indeed, the industry is seeing a “pricing reset” in 2026 where sellers either sell at full price for premium items or offer extreme markdowns to move inventory, with little in-between.

4. Beauty & Personal Care

The beauty industry remains a star performer online, combining high margins with passionate consumer engagement. In 2024, beauty and personal care e-commerce revenues were about $169.6 billion globally. Unlike apparel, beauty products (skincare, cosmetics, fragrances) typically have lower return rates (around 5%) and are consumable, leading to repeat purchases. By 2026, the “wellness boom” (more on that trend later) means beauty and self-care are only growing. One fascinating insight: beauty has been a margin stabilizer even in volatile times – while categories like fashion and home often resort to 50–80% discounts to clear stock, beauty has historically capped discounts around 25%. Consumers rarely expect makeup or skincare to be 70% off; brand loyalty and the “Lipstick Effect” (people treat themselves to small luxuries in downturns) keep this sector resilient. However, competition is intensifying: our forecast expects a 15% increase in fashion or lifestyle brands launching their own beauty lines in 2026 (everyone from apparel brands to influencers are adding cosmetics or skincare products). This could push beauty discounts slightly higher by late 2026 (possibly 30–35% off at times) as the market becomes more crowded. Key subcategories like skincare, clean beauty, and male grooming are expanding fast. Also, beauty is heavily driven by social media trends – a single viral TikTok (e.g. a unique lipstick or skin serum) can sell out product lines in days. For instance, a Wonderskin lip stain went viral on TikTok Shop, selling one unit every 5 seconds at its peak and over 300,000 units in 2024. Sellers in this space should be agile with influencer partnerships and limited drops to capitalize on surges in demand.

5. Health & Fitness

Closely related to wellness, the health & fitness category online has surged and will be a significant contributor in 2026. This includes vitamins and supplements, fitness equipment, and health gadgets. In 2024, online sales of health and fitness products (e.g. home gym equipment, nutrition supplements) were notable – for example, fitness trackers, yoga mats, and supplements drove an estimated 600 million units sold globally. Consumers’ heightened health awareness (partly a pandemic legacy) is here to stay. Expect Q1 2026 to kick off with strong sales in this category (New Year’s resolutions often lead to spikes in exercise gear and diet program sales – more on seasonality later). By 2026, we also include emerging “tech-driven” health products: think smartwatches with advanced health monitoring, at-home medical testing kits, and even AI-powered fitness apps (often sold via subscriptions). Another growth area is personal health devices (for example, massage guns, posture correctors, or even heated jackets for outdoor exercise – one trending product in 2025 was a 12V heated jacket catering to wellness and comfort seekers). Online penetration is increasing for health products that traditionally were bought in pharmacies or sports stores. For instance, consumers are now very comfortable buying supplements from online marketplaces or DTC vitamin brands; liquid multivitamins and wellness tonics have gone viral via influencer marketing, racking up tens of millions in sales on platforms like TikTok Shop. Overall, health & fitness intersects with both the beauty and consumer electronics realms (wearables, anyone?), making it a dynamic, fast-growing category to watch.

6. Other Noteworthy Categories

Several smaller (by revenue) categories are nonetheless important due to high growth or strategic value:

- Pharmaceuticals: Online pharmacies and telehealth services boomed recently. While pharma e-commerce wasn’t among the top 5 by revenue in 2024, it is reportedly the fastest-growing e-commerce segment globally. By 2026, more consumers (especially in North America and Europe) will be refilling prescriptions or ordering OTC medications online. Regulatory changes and digital health adoption are key drivers. Sellers in health adjacencies (e.g. wellness devices, medical supplies) will benefit from this trend.

- Media & Entertainment: This category (books, music, gaming, digital content) was about $194 billion in 2024 online. Physical media sales have shifted online (Amazon started with books, after all), but much of media is now digital (streaming, e-books). By 2026, physical media is a niche, but gaming merchandise, collectibles, and the like still sell. Also, toys and games ($89.8 billion online in 2024) remains relevant – especially during holidays – though many toy purchases happen on marketplaces under the broader “general merchandise” umbrella.

- Luxury Goods: Luxury is a smaller slice of e-commerce but growing as high-end brands embrace online channels. In the U.S., luxury goods accounted for about $14.9 billion in 2024 online sales. By 2026, expect luxury e-commerce to expand in China and the Middle East in particular. However, many luxury brands maintain exclusivity by limiting online distribution or keeping prices full – a dynamic described by the “platform specialization” trend (some sites focus on full-price luxury, while others handle discount outlets).

- Pet Supplies: The pet products market (pet food, pet tech, accessories) has quietly become a multi-billion dollar online category, especially in markets like the US and Europe where pet ownership is high. Auto-ship pet food and online vet care are trends boosting this segment in 2026.

- Tobacco Alternatives: E-cigarettes and vape products were listed at ~$116.6 billion online in 2024. Regulation will determine growth here, but there’s a notable online subculture around these products.

In summary, electronics and fashion will likely remain the top two online sales categories in 2026, with food/grocery challenging for the #3 spot (and possibly overtaking some others given its rapid growth). Home goods and beauty round out the top five in most markets, each with their own growth narratives. The key for sellers is not just to know which categories are big, but also how consumer preferences within those categories are changing. For example, within electronics, 2026 might be the year of mainstream AR/VR devices; within fashion, perhaps a resurgence of Y2K styles or sustainable fabrics leads the charge. Keeping an eye on breakout niches (e.g. the rise of collectibles in fashion or the fusion of health and tech in wearables) is important, since breakout items can lift entire categories. As we move to platform-specific analysis, we’ll see how different sales channels have unique category strengths – and how predictive intelligence can help forecast quarterly trends for these product types through the year.

Platform-Specific Breakdowns: Amazon, TikTok Shop, Shopify, and Temu

Not all e-commerce is created equal – each platform has its own ecosystem of products, buyers, and selling strategies. A product that’s a top-seller on Amazon might flop on TikTok Shop, and vice versa. In 2026, four platforms will be especially influential for online sellers:

Amazon: The Everything Store’s Best-Sellers

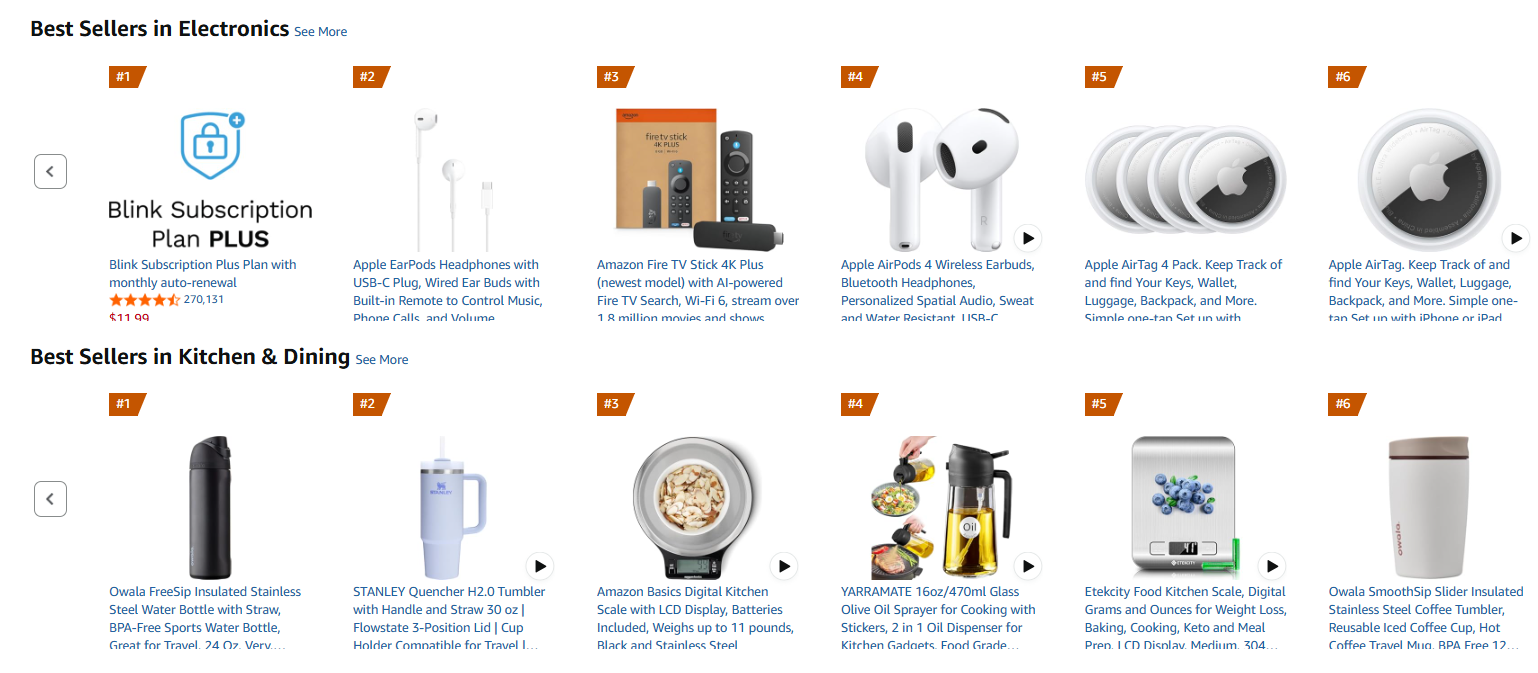

Amazon remains the juggernaut of e-commerce in the US and many Western markets, and it’s a major player globally. Often dubbed “the Everything Store,” Amazon’s marketplace truly sells almost anything. This breadth is reflected in its best-selling categories and products. According to surveys of Amazon sellers, the most popular categories that merchants focus on include Home & Kitchen, Beauty & Personal Care, Clothing & Shoes, Toys & Games, and Health & Household, among others. In fact, in 2024 about 35% of Amazon (U.S.) third-party sellers offered products in Home & Kitchen, making it the top category by seller participation, followed by beauty (26% of sellers) and apparel (20%). This aligns with consumer demand: home and everyday goods do extremely well on Amazon due to the convenience factor (Prime free shipping on bulky home items is a big draw) and Amazon’s recommendation engine surfacing household essentials.

When we look at Amazon’s best-selling products, the diversity is striking. A snapshot of the Top 25 Amazon best sellers in late 2025 included items ranging from Apple’s latest MacBook Air and Samsung 4K TVs to mundane staples like printer paper, toilet paper, and baby diapers. For example, in one monthly ranking, Apple laptops and iPads occupied several spots (showcasing Amazon’s strength in consumer electronics), yet the #1 item was actually a pack of Amazon Basics copy paper. Other top sellers included a patio furniture set, Nespresso coffee pods, electrolyte drink mixes, Bounty paper towels, and protein shakes. This highlights two key strengths of Amazon’s platform: (1) it captures high-end, big-ticket purchases (like laptops) and low-cost everyday needs (like pantry goods and household supplies), and (2) it serves as a one-stop shop where consumers feel they can find any product they search for. In 2026, we expect Amazon’s best-seller lists to continue reflecting a mix of high-volume commodities and trending gadgets.

What sells best on Amazon and why? A few patterns are clear:

-

Electronics & Tech Accessories: Amazon built its early reputation in books, but by the 2010s it became the go-to for electronics. Shoppers trust Amazon for competitive prices on TVs, laptops, headphones, and phone accessories – often checking reviews and ratings from millions of customers. With fast shipping and easy returns, even expensive electronics feel safer to buy. In 2026, expect electronics (especially Amazon-exclusive tech deals) to top sales. Amazon’s holiday promotions like Prime Day and Black Friday heavily feature electronics, which is why, for instance, an Amazon listing for a 13-inch MacBook Air was among the top sellers in Nov 2025. Smart home devices (Alexa-powered Echo gadgets, Ring cameras) also sell strongly, aided by Amazon’s own ecosystem integration.

-

Home & Kitchen Appliances: This category consistently ranks #1 in Amazon’s seller surveys and sales. Amazon carries everything from kitchen gadgets that go viral (air fryers, Instant Pots) to furniture and décor. In 2025, air fryers and other kitchen tools were standout performers on Amazon Australia, for example. The success of items like the Stanley insulated tumbler (a trendy drinkware item) on Amazon – it sold 1.64 million units in 2024 on Amazon US – shows that even relatively niche home products can dominate when they catch on in social media and are readily available on Amazon. The platform’s powerful search and category ranking system means that if your product hits #1 in a home/kitchen subcategory, it can snowball with thousands of purchases a day. Consumers also rely on Amazon for home basics (cleaning supplies, organizers) via subscription and save programs.

-

Beauty & Personal Care: Amazon has rapidly grown its beauty offerings, including luxury beauty and an assortment of K-beauty, drugstore brands, and indie products. One of Amazon’s best-selling beauty items in 2024 was the Mighty Patch acne patches, with over 2.5 million units sold in a year. Shoppers enjoy finding viral TikTok beauty hits on Amazon for a quick purchase (often cheaper or faster than buying from the brand’s site). Additionally, daily necessities like shampoos, lotions, razors, etc., are steady sellers thanks to Amazon’s convenience. Beauty on Amazon succeeds when products have strong reviews and repeat purchase potential (subscribe & save for things like sunscreen or toothpaste). The only caveat is that some prestige beauty brands limit Amazon distribution to avoid discounting, but Amazon is still making inroads here.

-

Apparel and Accessories: Fashion is a tougher category for Amazon (due to fit and brand-driven shopping off Amazon). But it’s still significant: Clothing, Shoes & Jewelry is among the top categories by seller count. Amazon’s apparel sales tend to skew toward basics and affordable items – e.g., simple jewelry, socks, generic coats – and its own Amazon Essentials line. Yet, a few apparel items break out; for instance, a simple Hanes EcoSmart sweatshirt became the #1 apparel bestseller in late 2024, after a surge in sales and positive reviews pushed it up the ranks. Amazon has also become a force in luggage and travel accessories (with so many comparing options on price), evidenced by travel pillows and luggage scales making top-seller lists in some regions. In 2026, Amazon is investing further in fashion (with try-before-you-buy Prime Wardrobe, etc.), but its strength will remain in mid-market, utilitarian clothing unless it finds a way to crack high-fashion appeal.

-

Everyday Essentials (Health & Household): Amazon is arguably the largest online supermarket for non-perishable goods. Consumers purchase huge quantities of household staples: toilet paper, paper towels, detergents, vitamins, baby diapers, pet food, etc. In 2024, for example, Bounty paper towels on Amazon averaged nearly 200,000 sales per month and more than tripled in sales during Q4 – showing how people stock up during the holiday season or sales. Baby products like diapers were also top sellers (e.g., 87k monthly sales for a diaper product). This category sells well on Amazon because of trust (you know what you’re getting with branded essentials) and convenience (bulky items delivered to door). Also, pandemic-era habits of ordering toilet paper online have stuck. In 2026, we anticipate Amazon doubling down on subscriptions for these goods and using its data to keep customers in its ecosystem for essentials.

Why Amazon? Amazon’s success across such varied categories is due to a few factors: Prime’s free and fast shipping encourages impulse buys of cheap items and confidence in big items alike; Amazon’s search dominance means it’s often the first stop for product searches (more product searches start on Amazon than on Google); and the vast number of third-party sellers ensures that if something is trending anywhere, it will quickly be available on Amazon. The platform also excels in cross-selling: someone coming to buy a phone case might also add on headphones or a charger – boosting overall sales in multiple categories.

In 2026, Amazon’s marketplace is maturing. That means competition is fiercer, and brands are more protective of pricing. We’re seeing a strategic use of Amazon by brands: some treat it as a clearance channel, others as a flagship. For example, luxury department stores differ in Amazon strategy (Saks offloading discounted inventory vs. Nordstrom holding price integrity). Sellers should recognize Amazon can either be used to push volume (even at slim margins) or to reach the massive Prime customer base with select products.

One more trend on Amazon: growth of private labels and Amazon’s own brands. Amazon will continue promoting its in-house products (Amazon Basics, Solimo, etc.) which often rank high for commodity items due to low price and Amazon’s algorithmic advantage. Third-party sellers need to differentiate with unique products or strong branding because competing on price alone with Amazon’s own products is tough.

TikTok Shop: Viral Trends and Social Commerce Gold

TikTok Shop is the relative newcomer that’s rapidly reshaping e-commerce through social media influence. Launched in select markets in 2021 and expanded aggressively by 2023–2024, TikTok Shop integrates shopping directly into the TikTok app, turning viral videos into point-of-sale opportunities. By 2025, TikTok Shop reached an estimated $25 billion in global e-commerce sales, making it one of the fastest-growing commerce platforms ever. In the UK, TikTok Shop was noted as the fastest growing online retailer in 2024, and similar momentum is seen in Southeast Asia and the US.

What sells best on TikTok Shop? In a word: trends. The platform’s top-selling products tend to be those featured in viral videos, beauty tutorials, fashion hauls, or gadget demos that capture the community’s attention. According to market analysis, the leading TikTok Shop US categories in 2025 were Beauty & Personal Care, Women’s Fashion (apparel/underwear), Health & Wellness, Sports & Outdoor, and Electronics, which together made up over 40% of TikTok Shop US sales. The dominance of beauty and fashion isn’t surprising – TikTok’s user base (young and trend-conscious) consumes huge amounts of style and cosmetics content. For example, TikTok Shop’s #1 best-selling product in the US in 2025 was a “Stay-N-Peel” lip liner (a peel-off lip stain) that went viral; it generated over $46.6 million in sales. Other top TikTok Shop items included a popular neck firming cream (~$32 million) and a liquid multivitamin supplement (~$29.9 million) – indicating how beauty and wellness fads take off here. Notably, even a home gadget (a cordless vacuum) and a smart home camera cracked the TikTok top 5 with ~$25 million each in sales, showing that the platform isn’t only lipstick and leggings – a clever demo of a cleaning device or security cam can also catch fire.

The why behind TikTok Shop best-sellers lies in content-driven discovery. Products on TikTok sell when they are:

-

Demonstrable: People see the product in action in a short video. Think of a cosmetic showing a dramatic before/after, or a blender chopping something effortlessly. If it looks cool on video, it sells. For instance, trending items like the Ninja Blast portable blender saw an 1800% surge in orders after going viral in a TikTok video. Similarly, a Shark steam mop video led to a 5800% increase in orders over a short period – astonishing evidence of impulse buying triggered by TikTok content.

-

Backed by creators/influencers: TikTok’s creator community drives trust and desire. A skin serum recommended by a beauty influencer or a funny skit featuring a gadget can prompt thousands of fans to buy. Creator-led tutorials (e.g. “get ready with me” #GRWM videos) are especially effective in beauty and fashion. TikTok’s own data shows that short-form videos demonstrating real results – like skincare routines or clothing try-ons – convert viewers into buyers rapidly.

-

Affordable and impulse-friendly: TikTok popular items are often relatively low-priced, making them easy impulse buys. Many TikTok Shop best-sellers are under $50, and quite a few are under $20 (lip liners, small gadgets, etc.). This sweet spot encourages viewers to purchase immediately through the app without much second-guessing. Even higher-ticket items (like the vacuum) sell because they’re presented as solving a problem efficiently, and often they’re competitively priced or discounted during the stream.

-

Unique or hard-to-find elsewhere: Some products trend on TikTok because they’re novel. For example, quirky beauty tools or niche health supplements might not be mainstream retail hits yet, but TikTok surfaces them to millions. The platform has essentially turned niche products like toothpaste tablets or lymphatic drainage vibration plates into huge sellers by boosting their visibility. The listed top 10 TikTok Shop products of 2025 included items like NOBS zero-waste toothpaste tablets and a Merach vibration plate exercise machine – items many hadn’t heard of until they exploded on TikTok.

In 2026, TikTok Shop’s influence will only grow, especially as it expands in Western markets. We anticipate the platform will continue to excel in beauty, fashion, and small home gadgets. For example, TikTok UK’s Shopping Report noted how certain fashion trends (like nostalgic collectibles Labubu toys and comfy “dad jeans”) and beauty trends (like long-lasting lip stains) drove massive engagement and sales spikes. TikTok has a knack for creating microtrends (e.g. a certain shade of blush or a style of earring can become a nationwide craze in weeks). Sellers who ride these waves – by quickly sourcing or manufacturing the trending item – can make a killing. However, the lifecycle of TikTok trends can be short; viral products might be “hot” for a few months before the next thing comes along. This means agility is key for TikTok-focused sellers. Inventory management must be tight (to not overstock a fad that fades), and marketing needs to pivot with the trends.

Another aspect is live shopping. TikTok Shop heavily uses live-stream commerce, a model perfected in China. Charismatic hosts showcase dozens of products in a single session with time-limited deals, driving urgency. In Southeast Asia and China, TikTok live sales have broken records. By 2026, Western markets are catching on. Expect TikTok to run major live shopping events (possibly tied to holidays or hashtag challenges), during which top sellers will include special edition cosmetics, bundle deals on fashion, and gadget flash sales. These live events often push whatever category TikTok is promoting – for instance, a “Summer Must-Haves” live might vault swimwear or portable fans into the best-seller list that week.

Why TikTok Shop matters to sellers: It represents the confluence of entertainment and shopping – so if you can create or market a product that’s entertaining or solving a relatable problem in a short video, you can tap into TikTok’s massive conversion engine. It’s particularly powerful for new or lesser-known brands. Many DTC brands that would struggle to get noticed on Google or Amazon can generate huge sales on TikTok by leveraging influencers or viral content. The platform also provides rich insights into youth culture and Gen Z behavior – what they buy often reflects emerging values (e.g. an emphasis on skincare health, or affinity for sustainably-packaged products, or just the meme-of-the-moment).

Shopify: DTC Brands and Niche Product Winners

Shopify isn’t a marketplace like Amazon or TikTok Shop; it’s an e-commerce platform powering millions of independent online stores. By 2025, Shopify reported hosting over 4 million active stores globally (and millions more have tried the platform). Collectively, Shopify merchants have facilitated about $1 trillion in online sales to date – roughly a 10% share of global e-commerce, showcasing Shopify’s immense footprint. The types of products that sell best on Shopify are often those tied to brand-driven, direct-to-consumer (DTC) trends. These are the products you see in Instagram ads or niche online boutiques, often with a unique twist or brand story.

Some defining characteristics of Shopify’s best-sellers and categories:

-

Apparel and Accessories dominate the Shopify landscape. About 28% of Shopify stores sell apparel products – by far the largest chunk for any category. This includes boutique fashion labels, print-on-demand t-shirt businesses, jewelry artisans, streetwear brands, and more. Many of the most successful Shopify stores are in the fashion space (for example, Gymshark in athletic wear, or Kylie Cosmetics in beauty, which is analogous to fashion in its marketing). Fashion and Shopify go hand-in-hand because the platform allows for beautiful, customized storefronts that reflect a brand’s identity – crucial for apparel where brand is everything. In 2026, expect independent fashion brands (especially those targeting specific niches like sustainable fashion, plus-size activewear, or cultural streetwear) to continue thriving on Shopify. The ability to build a community around a brand via social media and then funnel those customers to a Shopify site for purchase has been a proven formula.

-

Beauty and Wellness brands also shine on Shopify. Roughly 11% of Shopify stores are in the Beauty/Health/Fitness category. Many trendy skincare or supplement startups choose Shopify to sell directly to consumers. These products often rely on content marketing and influencer endorsements (which link directly to the brand’s Shopify site). For example, a natural skincare brand with a compelling founder story might get traction via TikTok or YouTube, then drive sales on their Shopify-powered website. Because Shopify doesn’t have a central marketplace, these brands often generate demand via social channels. The advantage is they own the customer relationship (email list, loyalty program, etc.) more than they would on Amazon. In 2026, look for more wellness products on Shopify – e.g. boutique vitamin regimens, personalized nutrition services, athleisure brands, etc. The wellness boom means even traditional categories (say, beverages) spawn DTC offshoots (like mushroom coffee or CBD-infused drinks sold on their own sites).

-

Home & Lifestyle goods are another key area. Around 12% of Shopify stores focus on Home & Garden products. These range from home décor artisans (handmade ceramics, woodwork) to innovative gadget creators (a startup selling a smart planter or an ergonomic pillow). Shopify is great for storytelling, and home product sellers often use that to their advantage – for instance, explaining how their kitchen tool is designed by chefs, or how their bedding uses ethically sourced materials. Many eco-friendly home products (reusable kitchenware, sustainable cleaning supplies) are sold via standalone Shopify sites, tapping into the sustainability trend with dedicated branding. In 2026, expect categories like home organization, eco-friendly swaps (like biodegradable household products), and smart home accessories from startups to be among Shopify’s strong performers.

-

Specialized niches and passion products: Some of the best-selling items on Shopify are those that fill a very specific niche and therefore face little competition on Amazon. For example, a brand selling only high-end cycling apparel, or a store dedicated to pet portrait paintings, or one that sells subscription boxes for a particular hobby – these flourish on Shopify because they can directly target the passionate communities for those niches. Consumers searching for these unique products often go straight to the brand site after discovering them on blogs or social media. Shopify’s flexibility (with apps for subscriptions, custom product builders, etc.) allows these sellers to create tailored experiences. In 2026, with consumer demand fragmenting into micro-niches, Shopify will empower thousands more micro-brand success stories.

-

High-value, design-centric products: Many premium brands use Shopify to ensure a slick, branded checkout. For instance, luxury or high-end direct brands (whether in fashion, electronics, or furniture) might avoid marketplaces to maintain pricing and image, choosing Shopify instead. As a result, you’ll find that Shopify merchants’ average order values can be higher in some segments. For example, a bespoke furniture maker or electronics startup (like a boutique audio equipment brand) likely sells via Shopify. Cartier, Tesla, and other big names have even used Shopify for limited releases or regional stores. In 2026, the trend of established brands launching direct sites (sometimes powered by Shopify Plus) will continue, meaning even more product categories (like high-end jewelry or auto accessories) are represented among Shopify sales.

To illustrate with data: Shopify’s 2025 statistics indicated that during the Black Friday Cyber Monday weekend, Shopify merchants collectively sold $9.3 billion (up 24% from the prior year). This massive figure – $4.2 million in sales per minute at peak – reflects a broad range of products, since it aggregates hundreds of thousands of stores. Top performers during such sales often include apparel, beauty products, electronics (especially from DTC electronics like headphones or accessories), and gift-worthy items across categories. The fact that 61 million consumers bought from Shopify-powered brands during that weekend shows that DTC brands have reach. Consumers often don’t realize they are buying “on Shopify,” they just know they’re buying from a brand’s site.

What sells best on Shopify in 2026 will align with general consumer trends but skew towards areas where brand differentiation is key. Some expected hot segments:

-

Sustainable and Ethical Products: Shopify brands often lead in sustainability because they can tell the story (e.g. using recycled materials, fair trade, donating proceeds). With 72% of global shoppers considering sustainability in purchases, Shopify sellers that highlight eco-friendly aspects (whether it’s fashion, home goods, or beauty) can capture conscientious consumers.

-

Personalized and Custom Goods: Be it customized jewelry, print-on-demand art, or personalized nutrition, Shopify stores can incorporate customization options (via plugins) to offer made-to-order items. Consumers love unique, personalized products – something marketplaces can’t do at scale. Expect this to drive sales in categories like gifts, apparel, and home décor on Shopify.

-

Bundle and Subscription Products: Many Shopify brands use subscriptions (for coffee, pet food, skincare regimens). These models, if successful, create recurring revenue and can make a product a best-seller by cumulative sales. A specific example might be a monthly wellness box or a refill plan for eco-friendly cleaning supplies – not a typical Amazon purchase, but flourishing on DTC sites.

-

Global and Regional Expansion of DTC: Shopify is international – top countries are the US (about 38% of stores), UK, Canada, Australia, and a growing presence in Asia and Latin America. In 2026, we’ll see more cross-border DTC selling. A K-beauty brand in Korea might sell to the US via Shopify, or a European artisan marketplace might spring up using Shopify’s multi-language capabilities. This means product diversity on Shopify will increase, but so will competition, as domestic brands face overseas niche competitors shipping globally.

It’s worth noting a meta-trend: Many brands use omnichannel strategies – selling on Shopify plus Amazon plus brick-and-mortar. By 2024, 90% of Shopify merchants were connected to two or more sales channels (social media, marketplaces, offline). So, what sells on Shopify might also appear on Amazon, but the approach differs. On Shopify, the brand can maintain pricing and collect customer data (emails for re-marketing). For example, a hit skincare product might rank on Amazon for convenience buyers, but the brand’s Shopify site might sell deluxe bundles or exclusive drops to loyalists.

Temu: The Budget Bazaar Goes Global

Temu is the rising star from the East shaking up global e-commerce with ultra-low prices and a treasure-hunt shopping experience. Launched in late 2022 by Pinduoduo (a major Chinese e-commerce firm), Temu expanded rapidly in the US, Europe, and other markets by positioning itself as a bargain hunter’s paradise, often compared to a mix of Wish, Shein, and dollar stores – all wrapped into a slick app with viral marketing. By 2025, Temu’s growth was staggering: it captured 24% of cross-border e-commerce sales worldwide in 2025, up from virtually 0% just two years prior. In other words, Temu went from unknown to matching Amazon’s share of cross-border parcel shipments by 2025. Its gross merchandise volume (GMV) soared 239% from 2023 to 2024, reaching $47.5 billion in GMV – an almost unheard-of growth trajectory.

What sells best on Temu? The platform is known for extremely low-priced goods, many sourced directly from Chinese manufacturers, across a wide array of categories. Key product categories and trends for Temu include:

-

Fashion and Accessories: Much like Shein, Temu offers incredibly cheap fashion items – from $5 dresses to $2 earrings. Clothing, shoes, jewelry, and accessories are big sellers as consumers (especially young shoppers) are enticed by the trendiness-to-price ratio. In Southeast Asia and Eastern Europe, Temu has gained popularity for fast-fashion alternatives at a fraction of typical retail prices. Look for seasonal fashion (e.g. summer swimwear, winter jackets) to do well, supported by Temu’s constant flash sales. In fact, one of Temu’s hot items in 2025 was a 12V heated jacket, tapping into both the winter apparel and wellness trend, which Temu sold far cheaper than specialty outdoor brands. The appeal of trying out new styles without spending much will keep fashion among Temu’s top categories in 2026.

-

Electronics and Gadgets: Temu’s electronics skew toward small, affordable gadgets and accessories – think wireless earbuds for $7, phone cases for $1, LED strip lights for $3, etc. Bluetooth headphones were highlighted as a high-demand item on Temu, with certain models selling in huge volumes. Consumers love these because they’re commodity tech items at rock-bottom prices (often unbranded or white-label products). Temu is also known for quirky electronics (like mini projectors, novelty USB gadgets, etc.) that gain attention on social media for being so cheap. While you won’t see $1000 phones sold much on Temu (people tend to trust established retailers for expensive electronics), you will see tons of accessories (chargers, smart watches clones, earphones) and low-cost devices. The connectivity and convenience trend drives this – everyone needs chargers and cables, and Temu undercuts even Amazon on those. In 2026, as more people hear of Temu, expect even greater volume in this category, potentially putting pressure on discount retailers elsewhere. Notably, Temu’s parent company’s expertise in gamified commerce means electronics often get promotional push (lotteries, group buys) to entice shoppers.

-

Home Goods and Decor: Temu carries myriad knick-knacks for home – organizers, kitchen tools, decorative lights, craft supplies – mostly priced a few dollars each. These impulse home buys do very well on Temu because they’re the kind of “I didn’t know I wanted that” items people add to cart given the low price. For example, things like automatic soap dispensers, peel-and-stick wall hooks, cheap throw pillow covers, etc., often trend on Temu. Since shipping is subsidized, even $1 items can be shipped, which is mind-blowing to consumers used to buying in $30 bundles elsewhere. In 2025, memory foam pillows and small kitchen gadgets were among hot items in some markets – likely Temu was a channel for some of those sales given its focus on value. By 2026, as inflation globally has pinched some consumers, Temu’s value proposition for home essentials (like a set of spatulas for $3, or LED string lights for $2) is very attractive. It’s essentially playing in the discount store/dollar store space but online. In fact, Temu already claims about an 11% market share of the US “discount store” retail category by 2025, behind only Dollar General and Dollar Tree – a remarkable feat showing it’s siphoning off dollar-store shoppers to online.

-

Beauty and Personal Care: While not as dominant as on TikTok, beauty products are present on Temu, especially low-cost tools (makeup brushes sets for $4, knock-off facial rollers, etc.) and some cosmetics. Consumers who might balk at unknown brands on their skin may still buy tools or accessories. Additionally, Temu sells a lot of nail art supplies, false eyelashes, and other beauty accessories popular among younger shoppers. The focus is again on cost – e.g., 10-sheet packs of face masks or generic K-beauty items at a few dollars each. A notable trend is that Temu (and sister Pinduoduo) tap into private label and factory-direct beauty. For instance, on the B2B side, tons of private label skincare and masks are being sourced (as shown by high sales volumes for vitamin C face masks in B2B stats), which often end up on consumer-facing platforms like Temu under various names. We can infer that by 2026, Temu will feature more house-brand or no-brand beauty products that mimic popular items but at a fraction of the price – e.g. a $5 collagen serum akin to a $50 one. It appeals to cost-conscious beauty enthusiasts.

-

Novelty and Trending Items: Temu is extremely reactive to trends. If something blows up on TikTok or in pop culture, Temu’s merchants often list a version quickly. Think of viral novelty items: e.g., during holiday seasons, a particular style of Christmas ornament or a Halloween costume accessory that trends – Temu will have it cheap. In 2025, Pitbull concert costumes and bucket hats trended in the UK after TikTok memes; while that example is specific, it shows how social memes drive shopping. Temu’s advantage is it can rapidly supply these trend-driven goods from Chinese factories. So in 2026, any meme or quick craze (for instance, a plush toy from a viral video, or accessories related to a new movie fandom) could see Temu as a key seller.

Why are these categories succeeding on Temu? Three main reasons:

-

Price, Price, Price: Temu’s core appeal is ultra-low prices, often with free shipping and discounts on first orders. It has trained shoppers to expect deals that undercut competitors by 30-50%. It achieves this by sourcing directly and subsidizing costs (often running at a loss to gain market share). For many basic products (phone cases, socks, kitchen towels), Temu is simply the cheapest option, period.

-

Gamified, Fun Shopping Experience: Temu’s app is designed to be engaging – flash sales, spin-the-wheel coupons, “complete the look” bundles, etc. This encourages add-on purchases. Someone might come to buy a cheap gadget and end up adding 10 other small items because why not at those prices. So, a broad range of categories benefit.

-

Aggressive Marketing and Customer Acquisition: Temu’s Super Bowl ad in Feb 2023 (“Shop like a billionaire”) put it on the map in the US, and since then it has aggressively acquired users. By 2025 it reportedly had over 1.2 billion app downloads and 530 million active users globally, thanks to continuous promotions. With that user base, Temu can push various category promotions to see what sticks.

In 2026, Temu’s trajectory suggests further expansion of its catalog and reach. It may push into groceries or consumables (there are hints of adding cheap packaged foods or household consumables, encroaching on dollar store territory further). It’s also likely to emphasize fast delivery in key markets as it grows logistics, which could let it sell more last-minute items (right now shipping can take 1-2 weeks; if that improves, even more categories like urgent need items could come into play).

For sellers and brands, Temu’s rise is two-sided: on one hand, it opens a huge new channel for volume, but on the other, it’s a race to the bottom on price. Many top-selling products on Temu are no-brand commodities where the platform or the factory, rather than an independent seller, might be capturing the margin. However, established brands might use Temu to liquidate inventory in international markets or to reach very price-sensitive segments without cannibalizing their main brand (similar to how some use dollar stores or outlets).

Regional E-Commerce Predictions: US, Europe, Southeast Asia, and Australia

Consumer preferences and best-selling products online can vary widely by region. Cultural differences, economic conditions, and local platforms all influence what sells and why in each market. Below we break down predictions and trends for 2026 in four key regions: the United States, Europe, Southeast Asia, and Australia. Each section highlights top product categories, growth areas, and unique consumer behaviors in that region.

1. United States: Innovation and Convenience Drive Top Categories

The United States is the world’s second-largest e-commerce market (after China), with online retail sales around $1.1 trillion in 2024 and growing steadily. American consumers are tech-savvy, accustomed to fast shipping (thanks to Amazon Prime and others), and have embraced online shopping across most product categories. The top-selling categories in the US closely mirror global trends, with a few distinctions in ranking and consumer behavior:

-

Fashion & Apparel is the #1 e-commerce category by revenue in the US, projected at $162.9 billion in 2024. Americans buy a lot of clothing and footwear online, from fast fashion to sneakers to luxury brands. Large retailers (like Amazon, which sells heaps of apparel basics) and specialty DTC brands together drive this. By 2026, expect fashion to remain on top, bolstered by ubiquitous online promotions and the ease of free returns which alleviate the risk of buying clothes without trying on. One nuance: the US market sees strong seasonality in fashion – back-to-school apparel and holiday season apparel spikes are notable. Also, niche segments like plus-size clothing, athleisure, and streetwear are thriving online, reflecting America’s diverse consumer base.

-

Consumer Electronics are immensely popular online in the US, but interestingly rank slightly below fashion in pure revenue. In 2024, electronics were around $120.1 billion in online sales (forecast), making it the third-largest US category after fashion and food. However, given high average prices, electronics significantly influence overall e-commerce value. By 2026, with new product cycles (e.g. next-gen gaming consoles, AR devices, smart home tech) and heavy competition among retailers, electronics online sales will further grow. American consumers are early adopters, so emerging tech (like AI-powered home robots or EV accessories) might become surprise best-sellers. The US also has large annual tech events (CES, Black Friday) that boost sales. It’s worth noting many Americans research electronics extensively online (reading reviews on Best Buy, Amazon, tech sites) before purchasing, so good content and ratings heavily sway what sells.

-

Food and Grocery ranks as the #2 category by revenue in the US e-commerce, at about $125.6 billion in 2024. This includes both groceries and takeout/delivery orders through apps. While online grocery is newer in the US compared to UK or China, it accelerated due to the pandemic and has become routine for many. By 2026, online grocery and food delivery will be even more ingrained – from weekly Walmart/Instacart orders to meal kit subscriptions. Key trends: rapid delivery services (15-minute grocery apps) have seen consolidation, but consumers still value speed – 82% of U.S. shoppers say faster delivery is a priority. Also, the rise of specialty online food (e.g. ordering farm-to-table or international snacks from e-com sites) adds to category growth. In terms of products, pantry staples, beverages (especially bulk buying via Amazon or Costco online), and pet foods are strong sellers online in the US. Health foods and supplements are also big in this channel.

-

Health & Personal Care (including wellness items) is another top category in the US, overlapping with food and beauty. Vitamins, OTC medicines, fitness gear, etc., see robust online sales. The US market has embraced wellness trends (protein powders, yoga equipment, mental wellness apps), so by 2026, products that tap into the enormous health-conscious consumer base (estimated 50%+ of U.S. adults actively try to eat healthy or exercise regularly) will do very well. For example, sales of fitness trackers and smartwatches remain high. Also, as noted earlier, online pharmacies and prescription services are expanding – by 2026, more Americans might refill meds through services like Amazon Pharmacy or others, boosting this category’s e-comm share.

-

Home Goods & Furniture perform well in the U.S. too – especially categories like small kitchen appliances (air fryers had a huge moment), home office furniture (standing desks, ergonomic chairs post-2020), and home décor. The U.S. has a culture of DIY and home improvement, so retailers like Home Depot and Lowe’s have invested in e-commerce; additionally, Wayfair and Overstock make furniture buying online mainstream. As housing markets fluctuate, so do big furniture purchases, but decor and smaller items sell year-round. One interesting data point: homewares and domestic appliances form the largest segment of online shopping in Australia – similarly, in the U.S., major appliance sales have shifted online significantly (people buy fridges and washing machines from websites after reading specs). By 2026, expect more integration of AR for furniture shopping and perhaps more bundled service (buy a BBQ grill online with assembly included, etc.) to drive sales.

-

Toys and Games see spikes during holidays. In the U.S., as of 2024, the toys/hobbies category online was smaller (~$21.2B), but it’s heavily seasonal (Q4 accounts for a large chunk due to Christmas). For 2026, one can predict that any given year’s hot toy (be it a new tech toy or a classic like LEGO) will largely sell online (parents have shifted to online shopping for convenience and finding deals). Also, the rise of adult hobbyist spending (e.g. collectibles, board games) has boosted this category around the year.

Unique U.S. market characteristics: Americans value convenience and speed – hence the proliferation of same-day delivery, easy returns (46% abandon purchases if return process is poor), and omnichannel options like buy-online-pickup-in-store (BOPIS). Price sensitivity exists, but U.S. consumers also love premium products and novelties (the US is a big market for early tech adopters and luxury buyers). Thus, both discounted goods and high-end goods sell, as long as the value proposition is clear.

Another factor is regional diversity within the US: urban areas skew more to e-commerce (people order groceries instead of driving in traffic), whereas rural areas might shop online for access to a wider range of products not available locally (so online could be the lifeline for specialty goods). By 2026, virtually all demographics are more comfortable with online shopping, including older consumers (boomers adopted e-commerce rapidly in early 2020s).

Platform influence: Amazon is dominant in the US, but other players matter too. Walmart’s online segment is growing (especially groceries). Niche sites and brand.com (Shopify sites) capture the high-end or specialized sales. Social commerce (Instagram, TikTok) is rising but still maybe <10% of US e-commerce by 2026 (though growing). It’s forecasted that by 2025, social media could account for at least 20% of US e-commerce sales, fueled by impulse buys and younger shoppers. This means viral items can explode in the US as well, like the famous example of a TikTok-viral cleaning product (Pink Stuff cleaner) that became a top seller on Amazon for weeks.

Outlook: The U.S. e-commerce market in 2026 will continue to be a bellwether for global trends, with AI-driven personalization (recommendations on Amazon or Netflix-style suggestions on shopping sites) playing a role in what people buy. Key macro trends like sustainability will influence purchases too: surveys indicate a majority of American consumers prefer brands with sustainable practices or packaging. For example, by 2026 more products marketed as eco-friendly (like biodegradable packaging, ethically sourced materials) will climb the best-seller ranks in categories like beauty, cleaning supplies, and fashion, reflecting consumer values.

2. Europe: Fragmented Markets Unified by Top Categories

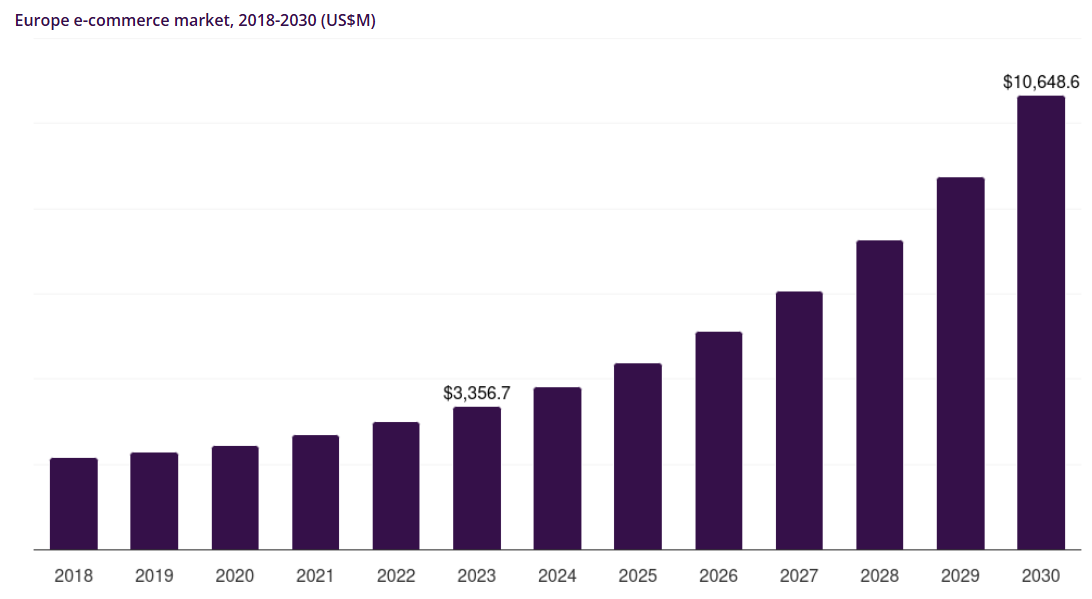

Europe’s e-commerce landscape is diverse, spanning mature markets like the UK and Germany and rapidly growing ones like Spain, Italy, and Eastern Europe. In 2025, Europe’s total e-commerce revenue was substantial (the EU and UK combined are second only to China/US as a bloc). A report projected Italy reaching $50 billion and Spain $60 billion in online sales by 2025, with over 70% of Spanish consumers shopping online – indicating how even traditionally lower e-com penetration countries are catching up. Across Europe, top categories in 2026 will include electronics, fashion, home goods, health/beauty, similar to global patterns. But regional preferences and the multi-country makeup add nuance:

-

Fashion and Apparel is a leading category in Europe, as it is globally. European online fashion sales are boosted by fast-fashion giants (Zara, H&M have strong online operations), luxury brands expanding direct e-com (Europe is home to many luxury maisons now selling online), and cross-border fashion (consumers buying from ASOS in the UK, or Zalando across EU). A European twist is that country styles differ – e.g., Italian and French consumers might spend more on high-end fashion online, while UK and German consumers are big on fast fashion and sportswear. Overall, clothing is hugely popular online Europe-wide, especially as free returns have become standard (Zalando pioneered that, making it low-risk to buy clothes). By 2026, even more of Europe’s apparel shopping will shift online, possibly aided by virtual fitting tech and more conscious consumer behavior (like buying secondhand or sustainable fashion on platforms like Vinted or Depop, which are popular in Europe). But in terms of new product sales, mainstream fashion and footwear will top the charts. For example, sneakers and streetwear are pan-European obsessions that sell briskly online, and seasonal fashion peaks around spring (for summer collections) and fall (for winter collections).

-

Electronics and Appliances are very strong online in Europe. Many European countries have high VAT on electronics in stores, so consumers often search for deals online. Leading categories include smartphones, laptops, and kitchen appliances. Interestingly, according to Ecommerce Europe, top categories by share of online shoppers include clothing and electronics, but also cultural goods and appliances. By 2026, as Europe rolls out 5G and other tech infra, we foresee continued strength in smartphones (with a big upgrade cycle expected as new models and perhaps AR glasses come mainstream). Also, Europe has a niche of specialty electronics – for instance, Germany has many hobbyist electronics and computer part shoppers (Mindfactory, etc.), and the UK has a strong console gaming market. These contribute to making electronics a staple online category. The rise of smart home devices and DIY electronics kits could also feature among best-sellers, tapping into consumer interest in energy saving (smart thermostats, etc., are big in Europe where energy costs are high).

-

Home Goods & Furniture show robust online growth in Europe. Furniture e-commerce was initially slow to take off (Europeans traditionally liked in-store furniture shopping), but companies like IKEA massively improved online shopping, and newer online-only players emerged. Home décor and small furnishings sell particularly well (e.g., lighting fixtures, linens, and kitchenware). Regional flavor: Northern Europe (Scandinavia) embraces online home shopping a lot, while Southern Europe a bit less but catching up. DIY is a major trend (think of all the IKEA hacks). By 2026, as younger generations (who are digital natives) become primary home-buyers/renters, they will buy much of their home furnishings online. Also, Europe’s emphasis on sustainability means that energy-efficient appliances and eco-friendly home products (like water-saving gadgets, solar lights) can be top sellers. In fact, household appliances and homewares have been the largest segment of online retail in countries like Australia (and similarly significant in Europe), showing that people appreciate the convenience of ordering bulky items online with delivery.

-

Health, Beauty & Personal Care: European consumers are quite health-conscious and also have strong beauty markets (France, Italy famous for cosmetics and skincare). Online sales of beauty in Europe are propelled by multi-brand retailers (Sephora, Douglas, etc.) as well as direct brands. By 2026, expect skincare to be a particularly hot segment (as it is globally), with many European consumers seeking out both dermatologist-approved brands and trendy K-beauty or natural products online. Additionally, pharmacy items in some European countries can be sold online (with regulation): e-pharmacies in Germany, UK, etc., have grown. Vitamins and supplements are moderately popular (less so than in US, but growing as wellness trends globalize). A key trend is sustainable and clean beauty – Europeans, especially in markets like France and Nordic countries, show growing preference for clean ingredients and eco-friendly packaging. Brands highlighting those features likely see e-com bumps (for example, L’Oreal’s waterless shampoo bars or refillable cosmetics might gain traction).

-

Groceries and Food Delivery: Europe is a bit behind the US in online grocery in some areas, but leading in others (the UK has had online grocery for over 20 years via Tesco). In 2026, as more Europeans get used to ordering groceries online (especially post-COVID behavior change), this will be a top category by sheer volume (though margins are slim). Unique to Europe are cross-border specialty food orders – e.g., someone in Germany ordering Italian wines or Spanish ham from an online specialist – which adds a gourmet dimension to e-commerce. Also, meal kit and quick delivery startups have proliferated (Gorillas, Flink, Getir in various countries). Their future in 2026 might consolidate but the demand for quick convenience remains. Expect grocery e-com to focus on urban centers and affluent consumers primarily, whereas rural uptake is slower due to logistics.

-

Cultural products (Books, Music) and Recreation: Europe has high readership, and Amazon started in books, so of course books remain a significant online seller. E-books and physical book e-com (e.g., via Amazon or local bookstore sites) will continue. Also, sports equipment (bicycles, outdoor gear) sells well online especially in northern and western Europe where outdoor hobbies are popular. For instance, Decathlon (sports retailer) sees much of its sales shifting online. In 2026, with maybe an Euro Cup football tournament or Olympics on the horizon, sporting goods could see regional spikes.

Europe’s regional complexity: Europe isn’t one homogenous market. Language, currency, and logistics differences fragment it. Local marketplaces still matter (e.g., Otto in Germany, Cdiscount in France, Allegro in Poland). However, the big players like Amazon, Zalando, and AliExpress have pan-European presence. Cross-border e-commerce is significant: consumers often order from other EU countries if prices are better. It was noted that the European cross-border market reached €358.7B in 2024/25. Temu’s entry and Shein’s popularity also influence Europe – for example, Shein is extremely popular for budget fashion among European youth, meaning affordable apparel segment is partly captured by Chinese platforms.

Consumer values: Europeans generally value privacy (stringent data laws like GDPR) and sustainability. According to DHL, ~72% of global shoppers consider sustainability, and in Europe that tends to be even higher. So products that are eco-friendly could outperform. Also, Europeans are more price-sensitive on average than Americans, and historically like discount periods (like Singles’ Day, Black Friday have been imported, and traditional sales in January and summer). By 2026, Black Friday is as big in Europe as in the US, so Q4 category sales (especially electronics and fashion) will spike due to heavy promotions.

Prediction: Europe’s best-selling online products in 2026 will largely fall into Fashion, Electronics, and Home categories, with Beauty/Health closely following. The differences will be in brand landscape (more local European brands in mix), language-specific content (marketing and site localization affects what sells in each country), and perhaps slightly slower adoption of some trends (e.g. social commerce isn’t as dominant yet in Europe, though growing). But fundamentally, a top seller list in Europe might not look too different from a global one: smartphones, game consoles, sneakers, fast-fashion apparel, skincare products, and home gadgets are all likely to be present.

3. Southeast Asia: Mobile-First Market with Social Shopping Surges

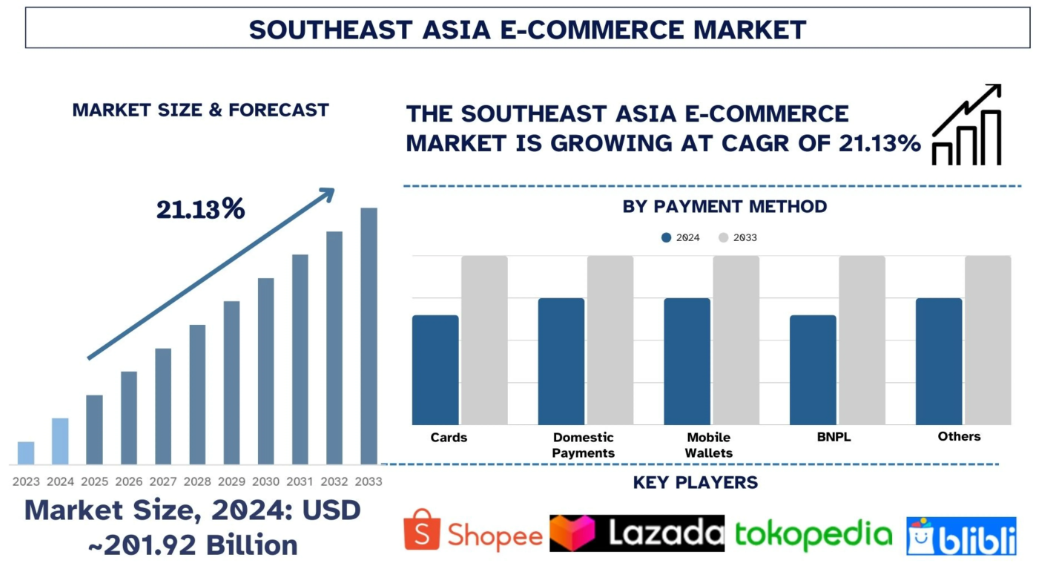

Southeast Asia (SEA) is one of the fastest-growing e-commerce regions in the world, encompassing countries like Indonesia, Thailand, Vietnam, Malaysia, Philippines, and Singapore. With a young population, increasing internet access, and a burgeoning middle class, SEA’s online market has boomed. Total e-commerce GMV in SEA was around $100 billion in 2024 and is projected to multiply over the next decade. Key characteristics: mobile-first consumption, a dominance of marketplaces (Shopee, Lazada, Tokopedia), and high social media usage impacting shopping.

Top product categories in SEA reflect both global trends and local nuances:

-

Fashion & Beauty reign supreme in many SEA markets. As noted, fashion, beauty products, and gadgets were the top categories region-wide. Affordable fashion is hugely popular – platforms like Shopee and Lazada often highlight flash sales for clothes, and Instagram boutiques are everywhere. Culturally, looking good is valued, and with a young demographic, there’s high spend on cosmetics, skincare (there’s a K-beauty and J-beauty influence), and trendy apparel. For example, modest fashion (like hijabs and Muslimah clothing) sells massively online in Indonesia and Malaysia; in Thailand, Korean-style fashion is in demand; in the Philippines, athleisure is a hit. By 2026, as incomes rise, we’ll see even more spending on fashion/beauty, including international brands entering via official online stores. But local sellers and inexpensive options still dominate (SEA consumers love a bargain and are used to price comparing across sellers on marketplaces).

-

Electronics & Mobile gadgets: Southeast Asians are heavy smartphone users and often use mobile as their primary internet device. Thus, smartphone sales and accessories are a big piece of e-commerce. Brands like Xiaomi, Oppo, Samsung do huge launch events online. Also, accessories like power banks, headphones, etc., are top sellers (partly because many SEA consumers have only moderate incomes, so they cherish and accessorize their phones heavily). By 2026, with more people upgrading to 5G phones and perhaps exploring devices like smartwatches or tablets for education, electronics stays hot. Affordable electronics in particular – SEA has many value-conscious shoppers, so mid-range smartphones (sub-$300) and knock-off gadgets sell strongly. Additionally, as digitalization continues, categories like laptops (for remote work/learning) and home appliances (like affordable air purifiers or kitchen appliances) are growing online.

-

Home & Living: In some SEA countries, this category is growing now from a smaller base. Urbanization and COVID (staying at home more) spurred interest in home goods. Shopee’s data often show home & living as a top category during specific campaigns (like 11.11 sale). Filipinos, for instance, got into home baking, so baking appliances sold a lot online. By 2026, expect further growth as more people become homeowners or improve their living spaces. Products like storage solutions, budget-friendly furniture, and home décor will find a ready market. One peculiarity: space can be limited in big cities, so multi-functional furniture or compact appliances might be particularly popular.

-

Health & Wellness: Southeast Asia faced the pandemic and came out with increased awareness of health. Sales of supplements, fitness gear (e.g., yoga mats, home exercise tools), and health foods have grown online. Traditional herbs and remedies are even being sold via e-commerce now. As we go into 2026, an emerging affluent class is investing in personal health – maybe buying smart fitness trackers, importing vitamins, or using apps that deliver healthy meals. While not yet the top category, health & wellness could climb in rank. Note that in many SEA countries, the average age is late 20s, so chronic health concerns are less prevalent than in older populations; however, they focus on fitness and beauty crossover (like collagen supplements, etc.).

-

Groceries & FMCG: Particularly in Singapore, online grocery is established (RedMart, etc.). In other SEA nations, it’s catching on (Grab, Gojek, etc., delivering groceries). Marketplaces have grocery sections too. By 2026, as infrastructure improves and trust builds, more people will buy packaged foods, household supplies, and even fresh produce via e-commerce, though it might still be a smaller share of total retail compared to Western markets. Nonetheless, items like baby products (diapers, formula) and bulk household goods are commonly ordered online by young urban families.

A defining feature of SEA e-commerce is the interplay of social media and marketplaces. Social commerce (live selling on Facebook, influencers on Instagram selling things) preceded formal e-commerce in some areas. TikTok Shop made an early push in SEA and saw major success (Indonesia was one of TikTok Shop’s first big markets). For example, live-stream selling of beauty products or fashion can draw tens of thousands of viewers in Indonesia, converting to instant sales. By 2025, some estimates had social commerce accounting for a significant chunk of sales in SEA. So by 2026, impulse buys via social platforms will heavily influence top sellers – a lipstick brand can go from unknown to top-selling in a week after a TikTok trend, similar to what we discussed globally but even more intensified in SEA due to cultural norms of shopping via chat and live streams.

Payments and trust: Many SEA consumers didn’t have credit cards, so cash on delivery was common. But now digital wallets (like ShopeePay, GoPay) and BNPL are widespread. The quote “mobile-first market with fast adoption of digital wallets” highlights that. This means more people can transact easily online, boosting all product categories. However, trust in sellers is built via reviews and chat – top sellers often have to engage with customers directly (e.g., via WhatsApp or marketplace chat) to answer questions. Good customer service can elevate a seller’s rank.

Local nuances and best-sellers:

-

In Indonesia (the largest SEA market), top online items often include Muslim fashion, electronics, and increasingly cosmetics. The sheer volume of population means even niche products (like a particular style of sandal or a local coffee brand) can be a top seller by number of orders.

-

In Thailand, beauty (especially skin-whitening products historically, and more recently Korean cosmetics) and fashion are big; also decor and craft items.

-

Vietnam sees a lot of electronics and fashion sales online, and interestingly, a strong motorcycle accessory market (since bikes are main transport).

-

Malaysia: similarly fashion and electronics, but also health supplements (Malaysians are quite into vitamins and such).

-

Philippines: gadgets (Filipinos love tech and are heavy social media users) and fashion, plus imported goods that might not be in local stores.

-

Singapore: being wealthier, high-end electronics, branded fashion, groceries, and specialty items are big (many shop overseas sites too).

All told, Southeast Asia in 2026 will see fashion, beauty, and electronics as the top e-commerce categories, driven by a youthful, mobile-centric consumer base. Regional mega-sales (monthly double-digit date sales like 10.10, 11.11) will dictate spikes; during those, everything from diapers to smartphones sell in huge quantities due to steep discounts and gamified shopping rewards. The best-sellers often correspond to whatever promotions the marketplaces push (like “top-up your wardrobe sale” – clothing will surge, or a brand day for Samsung – phones surge). One thing to watch is cross-border Chinese platforms (like AliExpress, Shein, and now Temu) making more inroads, offering even cheaper goods – local players then respond by highlighting authenticity and local customer service.

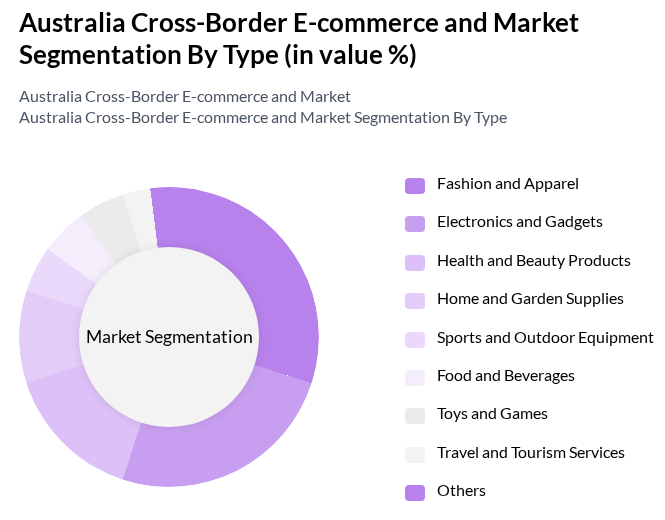

4. Australia: Health, Home, and the Amazon Effect

Australia’s e-commerce scene is somewhat unique – it’s a developed market with high internet use, but due to geography and a relatively small population (~26 million), its total e-commerce size is more modest (about AUD 63 billion in 2024, which is ~$45B USD, though growing). Still, Australians are avid online shoppers, especially given the wide distances (online can offer more variety than local stores for those outside major cities). By 2026, Australia’s online retail is well-established, with key categories being health & wellness, home goods, and fashion, among others.

Some trends and top-sellers in Australia:

-

Health & Wellness Boom: Australia has seen a surge in health and wellness product sales online. According to a recent analysis, products like toe spacers (for foot health) jumped 155% month-on-month, Pilates reformers up 53%, and various health supplements (minerals, herbal, protein powders) are surging in demand. This signals a strong post-pandemic wellness boom. By 2026, expect Australians to continue splurging on fitness gear (home gym equipment, running apparel), vitamins and organic foods, and wellness gadgets. Australia’s outdoorsy culture also means sports and outdoor recreation gear (like camping equipment, surf and swim gear) sell robustly online, especially as specialty retailers put inventory online. The “wellness boom” is also tied to beauty – Aussie consumers lean towards natural and sustainable products (the country has a lot of skincare brands touting botanicals, reef-safe sunscreen, etc. that do well online).

-

Home & Lifestyle Upgrades: With a lot of time at home in recent years, Aussies invested in their homes. Data from 2025 showed memory foam mattresses sales up 881% MoM and refrigerator accessories up 99% – huge spikes indicating a focus on home comfort and organization. Australians have relatively large homes and love home improvement (popular TV shows like The Block testify to that). Online, the top home products include small kitchen appliances (air fryers were big in Oz too), home décor, and DIY tools. Also, given Australia’s climate, outdoor furniture and BBQ equipment are popular in spring/summer. By quarter: Q4 and Q1 (summer holiday season in Australia) often sees high spending on outdoor living items, while mid-year might see more heating/bedding sales (it’s winter then). By 2026, smart home devices (security cameras, smart doorbells – a Wyze Cam was among TikTok top items in the US which likely similarly finds market in Australia) will be even more common as prices drop and awareness rises.

-

Seasonal and Back-to-School Trends: Australia’s seasonal pattern is opposite to the northern hemisphere, which affects e-commerce trends. For example, back-to-school is late January, and indeed in 2025 analysis, lunch box sets (+106% MoM) and school uniforms (+97% MoM) spiked during the back-to-school season. This will continue – every January, expect those items to top the charts as families prepare for the new school year. Likewise, end-of-year (Nov/Dec) is summer – so sales of swimwear, beach gear, and air conditioners surge. Australian e-tailers have begun to participate in Black Friday and Cyber Monday in November, which aligns awkwardly with summer, but nonetheless consumers buy a lot of electronics and gifts then. Also, there’s Click Frenzy (a big Aussie online sale event) and mid-year EOFY (end of financial year) sales in June, where tech and appliances deals abound (like Americans’ Black Friday).

-

Amazon’s Growing Role: Amazon launched in Australia only in 2017, but by 2025, 63% of Australians planned to shop on Amazon. It’s quickly become a major online retailer, leveraging fast delivery and a growing Prime membership. Amazon’s presence means product availability in Australia has widened, and prices became more competitive. Top Amazon.au categories mirror those in the US: Beauty & Personal Care, Home & Kitchen, Clothing, Toys, and Health were highlighted. For instance, top items on Amazon Australia in 2025 included everyday goods like soaps, shampoos, kitchen gadgets, travel accessories (pillows, luggage scales), educational toys, and household supplies (toilet tissue, dishwashing tabs). This suggests Australians use Amazon for both essentials and specialty items. By 2026, Amazon may introduce more of its own devices (Echo, etc.) and subscriptions which could become hot sellers. Also, Amazon’s “Haul” storefront (a budget-focused section) was attracting thrifty shoppers. So we might see more lower-cost fashion and home items trending via Amazon as well.

-

Local Retailers Online: Traditional Aussie retailers (e.g. Kmart, JB Hi-Fi, Woolworths) have improved their online stores. JB Hi-Fi (electronics) often leads in gadget sales – by 2026, new console releases or iPhones will have strong pre-orders online through such retailers. Supermarkets doing delivery means top-selling online groceries are items like bulk beverages, pet food, and household cleaners, often ordered by families.

-

Unique to Australia: Certain products like eco-friendly and wellness goods resonate (Australians generally are environmentally conscious). For instance, demand for sustainable products (like reusable cups, green skincare) is notable. Also, Australia’s geography means e-commerce is a boon for remote areas – someone in the Outback can now get products delivered that previously took long drives. So we might see some unique best-sellers such as water filters or solar chargers among rural online shoppers. Additionally, Australia’s strong cosmetic/skincare industry (lots of local brands like Aesop, etc.) means health/beauty exports are big; domestically, consumers buy those as well as imported brands online.

Australia’s consumers have high expectations similar to Americans: fast shipping (though given distances, 2-day delivery may only be in metro areas), easy returns, and good customer service. According to analysis, 82% of Aussie shoppers prioritize fast delivery, and 46% abandon carts over poor returns. Retailers are responding with better logistics. By 2026, innovations like drone delivery might even start in parts of Australia (there have been trials).

Regional predictions: In 2026, the best-selling online products in Australia will likely revolve around:

-

Health & personal care: including fitness gear, supplements, and maybe devices like massage guns (wellness tech).

-

Home & garden: especially items that enhance comfort or organization (mattresses, storage solutions) and seasonal yard/outdoor products.

-

Consumer tech: Australians love gadgets; expect strong sales for phones, headphones (perhaps noise-canceling headphones remain popular given travel and commuting culture), and gaming devices.

-

Fashion & kids products: Clothing does well, particularly casual and sportswear (big sports culture), and children’s products (toys, baby items) see consistent demand.

One more macro: Australia’s macroeconomic environment – if the Australian dollar is weak, people might order locally rather than from overseas; if it’s strong, more cross-border shopping happens. But since our focus is internal market, currency mainly affects pricing of imported goods which most categories rely on.

Regional Outlook Summary: Despite cultural differences, e-commerce in the US, Europe, SEA, and Australia shares common top categories – fashion, electronics, home, and beauty/health consistently appear. The differences lie in consumer behavior (e.g., social commerce uptake, discount hunting, delivery expectations) and local trend flavors (e.g., modest fashion in SEA, luxury in Europe, wellness in Australia). By leveraging regional data and tailoring strategies to local preferences, sellers can tap into the hottest products for each market in 2026.

Quarterly Predictions for 2026: What’s Hot Each Quarter

Consumer interests aren’t static throughout the year – they ebb and flow with seasons, holidays, and cultural events. For 2026, we can anticipate distinct e-commerce trends in each quarter. Below is a quarter-by-quarter breakdown of trending product types and consumer behaviors, complete with key seasonal triggers and data-supported insights:

Q1 2026 (January – March): New Year, New Needs

Key Themes: Health kicks into high gear, post-holiday bargains, and (for some regions) preparing for spring.

-